With many people sending and receiving payments every day, payment has become a social infrastructure on the same level as water and electricity. Cashless methods have also become a normal means for in-store payments since the COVID-19 pandemic.

Many individuals have used cashless methods to pay companies. The second wave of cashless payments is here, as these methods are expanding to payments between companies. This business to business (B2B) market is over five times larger than the business to consumer (B2C) market. We spoke with Junichi Sakishima, corporate officer of Digital Garage, Inc. (DG), about the possibilities of this business that is drawing worldwide

Speaker

Head of the Incubation Division; Corporate Officer; Digital Garage, Inc

Junichi Sakishima

At Mitsui & Co., Ltd., his job included Fintech investment and business development in Tokyo, New York, and London. Afterwards, he played a leading role in reforming the global supply chain at FAST RETAILING CO., LTD. Sakishima joined Digital Garage, Inc. in 2022 as corporate officer.

Major room for growth in the B2B cashless payment market

So, what exactly is a payment? Gottfried Leibbrandt, former McKinsey & Company partner and former CEO of SWIFT, said that a payment is a method for discharging debts. Payments were handled by banks and via cash in the past, but today credit cards and their companies are gaining prominence. Mobile payments are also coming into widespread use in recent years, such as PayPay and LINE Pay. Companies like Mercari and ZOZOTOWN are entering the financial service field for the first time. All these financial services discharge user debts in exchange for receiving handling fees from the payer or store.

Because payments are a regular part of daily life, success depends on the degree to which the service provider can offer better ease of use. Fintech has begun making major waves in the payment sector by adding payment functions to various types of services, and investors around the world are paying particular attention to Fintech companies. Corporations can no longer afford to ignore this business field, and there appears to be significant room for growth in Japan.

“It seems like cashless payments are widespread in Japan using mobile devices or credit cards, but that’s not yet the case,” said Sakishima. “The B2C market is roughly 300 trillion yen, of which cashless payments make up one third at about 100 trillion yen. Most of these are credit card payments. The B2B market has a larger scale at 1,700 trillion yen, yet credit card payments account for just five trillion yen.”

This disparity suggests latent room for cashless growth in the B2B market, which is the target of great expectations for further development.

Multi-industry growth for cashless payments, which can improve cashflow and management efficiency

On the topic of how cashless payments will expand in the B2B market, Sakishima said, “A major B2B payment revolution is imminent due to increasing digitization.” After services are created to meet digitization needs for varied work tasks in different companies and industries, cashless payments are incorporated into these services.

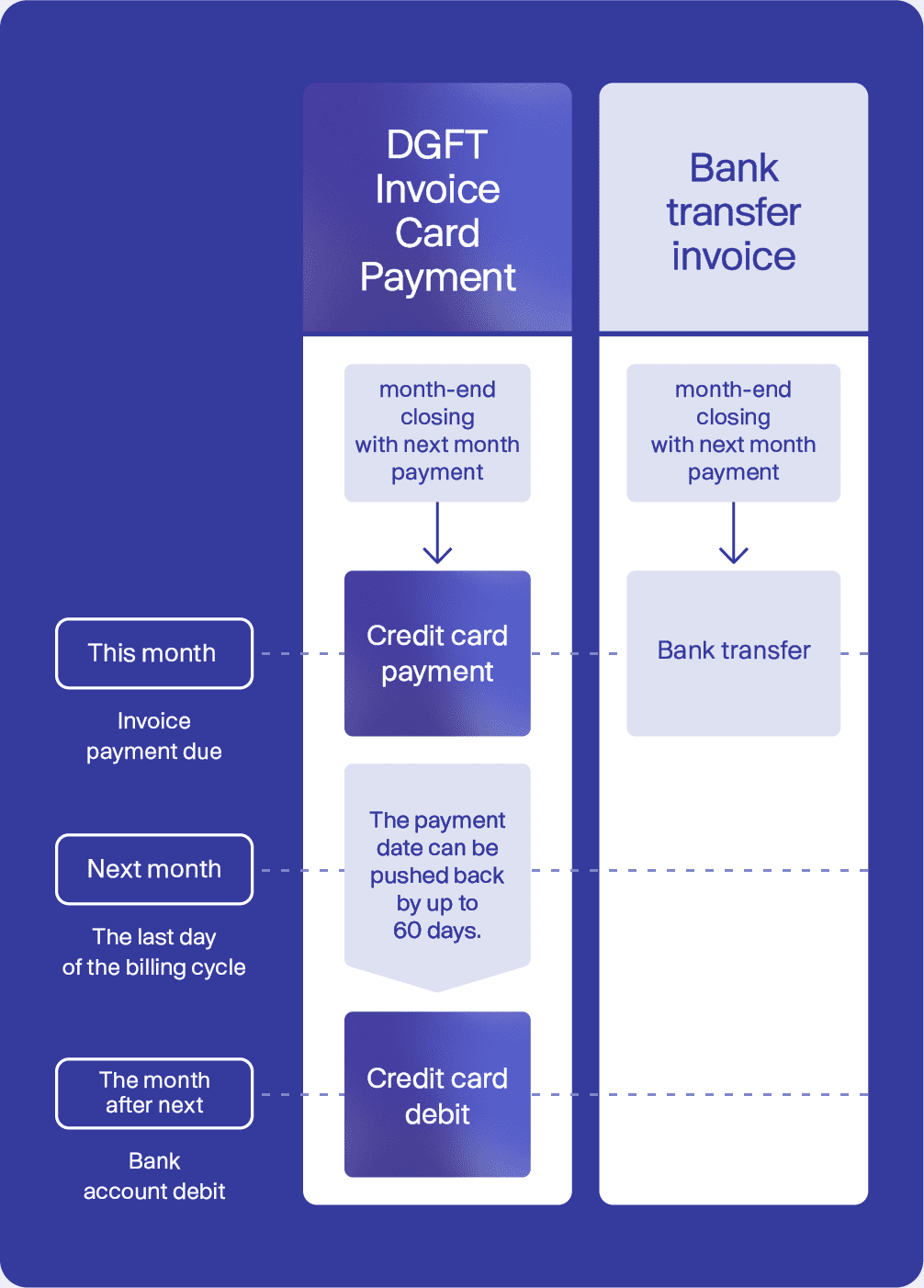

For example, Kakaku.com’s “Tabelog Shiire,” an ordering system for restaurants and wholesalers, includes a cashless payment service. Payments between business operators are generally completed by bank transfer invoice. With “Tabelog Shiire,” the business operator can select cashless payments to effectively postpone the payment due date by up to 60 days, which can improve seasonal cashflow issues and boost management efficiency.

Cashless payments have also spread to the construction industry, which has multilayered, complex supply chains due to the many companies involved from design to management. “GACCI,” which increases the efficiency of price quoting between construction business operators, now offers a credit card payment function for B2B transactions.

For transactions between companies, the regular process involves the contractor sending an invoice to the project operator with the agreed-upon price. The project operator pays the amount to the contractor’s bank account by the specified deadline. Although more companies are using digital quotes and invoices, few have implemented cashless payments because it is difficult to change existing business practices.

As the “Tabelog Shiire,” and “GACCI” examples demonstrate, the most important point in the B2B market is that digital work tasks and services can lead to the use of digital payments.

B2B payment systems are expected to keep evolving along with future waves of digitization. Sakishima said, “DG has been involved in the payment business for a long time. We will partner with companies that have yet to enter the payment field. We will also collaborate with software as a service (SaaS) businesses, startups, credit card companies, financial institutions, and other corporations.”

Growing Fintech potential with cashless payments

New attention is focused on the potential of credit card payments in the B2B cashless payment field. Credit cards have been around for roughly 50 years, and today they are accepted at two thirds of stores with approximately 10,000 credit card payments every second. This global payment method has an annual growth rate of more than 10%. However, Sakishima said, “I think there is still space in the market for credit cards to demonstrate further potential.”

This is because most credit card payment systems are used in scenarios based on B2C market needs. Currently, stores and other facilities that accept credit card payments must register to implement these payment systems. The credit card company receives a handling fee from the store. It is difficult to apply this method to the B2B market, where companies receive no benefits from paying handling fees to take credit card payments.

This has led to new B2B payment services that allow either party to bear the cost of handling fees, according to business practices and relationships between buyers and sellers. When the buyer pays this fee, the service can help improve their cash management. When the seller pays, it is like they are using a factoring-style financial service. This payment method is convenient and logical for both parties, and this convenient service offers advantages for both sides. The payer does not need to complete bank transfer procedures, resulting in an easier process and simpler payment cycle management. The payee no longer has to complete a complex registration process and can spend less time worrying about checking for anti-social forces or money laundering. B2B credit card payments have been started in other countries and are already utilized in Japan.

One barrier is the need to change existing payment practices. However, companies can be encouraged to use cashless payments by pointing out that digital work tasks and services can lead to digital payments as well. The increasing use of B2B credit card payments is sure to become a turning point for the industry.

Further business growth should be possible if cashless payments are included in B2B digital services. Besides payments, companies could offer new financial services by obtaining data from digital services about customer money and product trends. With major room for growth in the B2B Fintech market, DG is working to cultivate new services that can bring about major changes in all industries.